If you’ve opened your auto insurance renewal lately, you probably did a double-take. Across North Carolina, drivers have noticed their premiums shifting, leading many to ask a frustrating but fair question: “What exactly am I paying for, and do I really need all of it?”.

As we head into 2026, the conversation around full coverage has changed. It’s no longer just about picking a plan and forgetting it; it’s about understanding how modern vehicle technology, rising repair costs, and new state laws impact your wallet. Whether you are commuting to Fort Bragg or navigating the tree-lined streets of Haymount, this guide will help you determine the right level of protection for your lifestyle without overpaying for “fluff”.

Understanding the “Full Coverage” Myth and 2026 Realities

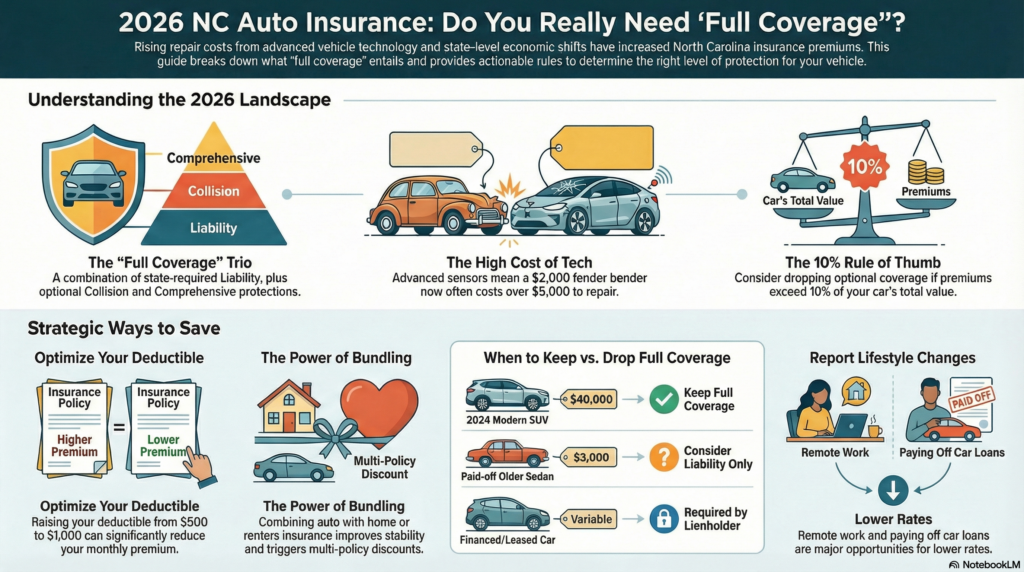

The term “full coverage” is actually a bit of a misnomer in the insurance world. Usually, when people say they want full coverage, they mean a policy that includes liability, collision, and comprehensive protections.

The Breakdown of Your Policy

To decide if you need the whole package, you first have to know what each piece does:

- Liability Coverage: This is required by North Carolina law. It protects your assets if you are found legally responsible for an accident that injures someone else or damages their property.

- Collision Coverage: This pays to repair or replace your vehicle if you’re involved in a crash, regardless of who is at fault.

- Comprehensive Coverage: Think of this as “everything else” coverage. It handles damage from theft, vandalism, fire, or “acts of God” like falling branches or hail.

Why Costs Increased in 2025

If your rates went up recently even without a claim, you aren’t alone. In 2025, several factors pushed prices higher:

- Higher Repair Costs: Modern cars are packed with advanced driver-assistance systems (ADAS) sensors in bumpers and windshields. A minor fender bender that once cost $2,000 to fix can now easily exceed $5,000 because of the required calibrations.

- Elevated Vehicle Values: While used car prices have cooled slightly, they remain significantly higher than pre-2020 levels, which increases total loss payouts for insurers.

- State-Level Pressure: In North Carolina, insurers have had to adjust pricing to maintain adequate reserves after years of absorbing losses.

For more information visit the NHTSA Safety Website.

The 2026 Underwriting Shift

In 2026, insurers are focusing less on “who” you are and more on how you manage risk. Predictability is the name of the game. Carriers are placing more weight on clean driving records and multi-policy household structures.

When to Keep Full Coverage (And When to Drop It)

Deciding to keep or drop full coverage isn’t a one-size-fits-all choice. It depends on your vehicle’s value, your financial “cushion,” and your specific loan requirements.

The “Lienholder” Rule

If you are financing or leasing your car, the decision is usually made for you. Most lenders require you to carry both collision and comprehensive coverage to protect their investment until the loan is paid off.

The 10% Rule of Thumb

A common neighborly tip is the “10% rule.” If the annual cost of your collision and comprehensive coverage exceeds 10% of your car’s total book value, it might be time to consider dropping down to liability only.

- Scenario A: You drive a 2024 SUV valued at $40,000. Replacing that out of pocket after a total loss would be devastating. You absolutely need full coverage.

- Scenario B: You have an older, paid-off sedan worth $3,000. If the “full coverage” portion of your bill is $400 a year with a $1,000 deductible, you are paying a lot for very little potential payout.

Considering Your Deductible Strategy

If you want to keep the safety net but lower your premium, look at your deductibles. Raising a deductible from $500 to $1,000 can noticeably reduce your monthly cost. However, ensure you have that $1,000 tucked away in an emergency fund so a claim doesn’t become a financial crisis.

Controlling Your Costs in a Tight Market

You can’t control the global economy or the North Carolina Rate Bureau, but you can control how your policy is structured.

Strategic Bundling

Multi-policy discounts remain one of the most effective ways to offset rising auto premiums. Bundling your auto insurance with homeowners, renters, or even an umbrella policy not only saves money but often improves your “stability” in the eyes of an underwriter.

Lifestyle Changes That Matter

If your life has changed, your agent needs to know. You might be eligible for lower rates if you:

- Work Remotely: Reduced annual mileage often leads to lower premiums.

- Paid Off Your Loan: This removes the gap exposure and gives you the flexibility to adjust your coverage levels.

- Improved Your Credit: In many cases, an improved credit profile can lead to better insurance tiers.

What NOT to do in 2026

When prices rise, the temptation to “slash and burn” your policy is high. Avoid these common mistakes:

- Dropping Liability Limits to State Minimums: With medical and legal costs rising, state minimums often aren’t enough to protect your home or savings if you’re sued.

- Ignoring Coverage Reviews: “Set it and forget it” is a costly strategy in 2026. A 15-minute review can often uncover outdated info or missing discounts.

- Switching Purely on Price: Frequently hopping between carriers can actually make you look “risky” to insurers, potentially leading to higher rates in the long run.

Peace of Mind is the Priority

Ultimately, the goal of insurance isn’t just to satisfy a legal requirement—it’s to ensure that a bad Tuesday doesn’t ruin your financial future. Whether you choose to maintain full coverage or pivot to a more streamlined policy, the most important thing is that the choice is intentional.

As we navigate 2026, staying informed and proactive is your best defense against rising costs. By reviewing your vehicle values, adjusting your deductibles, and bundling your policies, you can find that “sweet spot” where you are properly protected without overpaying.

We are here to help!

If your auto insurance increased recently and you aren’t sure why, we are here to help. Whether you need a quick coverage review, want to explore bundling options, or just need a second set of eyes on your policy, reach out today. Let’s make sure you’re properly protected—not just the cheapest on the block.