Buying a home is one of the biggest milestones in life, and for our military community here in Fayetteville, it is an exciting journey that often comes with its own unique set of rhythms. Whether you are currently stationed at Fort Bragg or planning an upcoming PCS move, navigating the financing world can feel a bit overwhelming. We often think of home insurance or mortgage terms as things that are already “handled,” but the reality is that the real estate landscape—especially for VA loans in 2026—is a living part of your financial health that deserves a fresh look.

As we head into 2026, the Fort Bragg-area housing market (now Fort Bragg) is entering a period of relative stability compared to the dramatic price swings we see in national headlines. For our service members, veterans, and eligible surviving spouses, VA loans remain a powerful resource designed to help you achieve homeownership with favorable terms that simply aren’t found in conventional lending.

In this guide, we’re going to walk through the essential 2026 updates, the core benefits of your entitlement, and how to strategically use VA loans to build long-term stability for your family in North Carolina.

1. The Core Advantages of VA Loans in 2026

The VA loan was created back in 1944 to help returning service members buy homes without needing a mountain of cash or a “perfect” credit score. In 2026, these benefits are more relevant than ever, especially as we see moderating home prices and a more balanced inventory in the local market.

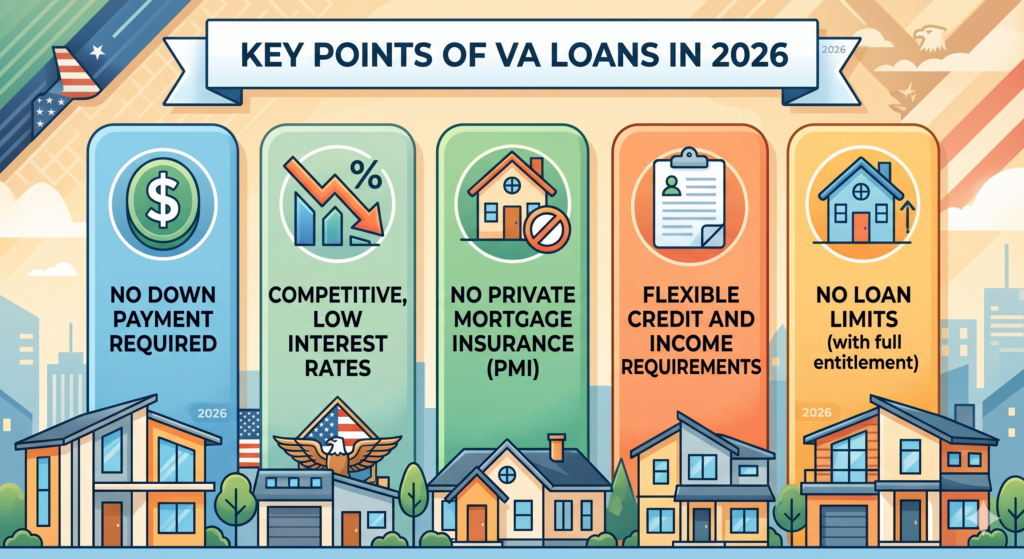

No Down Payment and Lower Monthly Costs

One of the most significant advantages for military buyers in Fayetteville is the ability to purchase a home with no down payment required. This can be a huge relief for families who would rather keep their savings for emergency funds or home improvements. Additionally, unlike conventional loans, VA loans do not require private mortgage insurance (PMI). This absence of PMI can save you hundreds of dollars every month, increasing your overall buying power.

Flexible Credit and Competitive Interest Rates

While we’ve seen interest rates stabilize after the fluctuations of recent years, VA loans typically offer lower interest rates compared to traditional financing. Lenders in 2026 also tend to have more flexible credit requirements. Most lenders prefer a score around 620, but because the VA guarantees a portion of the loan, there is often more room for negotiation and consideration of your full financial picture.

A Lifetime, Reusable Benefit

It is a common myth that you can only use your VA entitlement once. In reality, this is a lifetime benefit. If you’ve used a VA loan in the past, you can often restore your entitlement by selling the previous home and paying off the loan, or even use “remaining entitlement” to purchase a second home if you are relocating.

2. Navigating the 2026 Fayetteville Market Strategy

Success in the 2026 real estate market depends more on strategy and timing than on trying to “beat” the market. For VA buyers, the current environment offers something we haven’t seen in a while: a bit more leverage.

Sellers Are More Flexible

Because inventory has improved, sellers in the Fort Bragg area are becoming more willing to negotiate than they were during the “bidding war” years. We are seeing more sellers willing to:

- Cover closing costs, which the VA specifically allows and even limits for the buyer.

- Consider repairs discovered during inspections without the immediate threat of the deal falling through.

- Accept VA appraisals without the “pushback” or fear of strict Minimum Property Requirements (MPRs) that some sellers had in the past.

The Importance of the VA Appraisal and Inspection

It is crucial to remember that a VA appraisal is not the same as a home inspection. While the appraiser ensures the home meets the VA’s Minimum Property Requirements—meaning the home is safe, sound, and sanitary—it doesn’t go into the granular detail of a professional home inspection. Especially with historic homes in areas like Haymount, we always recommend a full inspection to uncover potential issues with older HVAC systems, roofs, or wiring before they become your responsibility.

Strategic Buying for Long-Term Stability

In 2026, we encourage military families to buy with a “long-term” mindset. If you plan to stay in the area for 3 to 5+ years, homeownership is an excellent way to build equity. Around Fort Bragg, rental demand remains consistently high due to the constant inflow of service members and limited on-post housing. This means that even if you receive PCS orders later, your home in Fayetteville often makes for a durable, long-term rental investment.

3. How to Get Started: The 2026 VA Loan Checklist

Starting your home search with a pre-approval is the best way to move with confidence. It shows sellers you are a serious buyer and gives you a clear, realistic budget so you don’t waste time on homes that aren’t a fit.

Step 1: Obtain a Certificate of Eligibility (COE)

The COE is the formal document from the VA that proves you are eligible for the benefit based on your service history. You can get this through the VA’s eBenefits portal, or often, your local lender can pull it for you in a matter of minutes.

Step 2: Work with a Military-Friendly Team

Choosing a real estate agent and a mortgage lender who understand the “military language” makes all the difference. A military-friendly realtor understands the stress of a tight PCS timeline and can help you navigate virtual tours if you are shopping from a distance.

Step 3: Factor in the “Full Cost” of Homeownership

When budgeting for your VA loan in 2026, don’t just look at the mortgage payment. Make sure to account for:

- Property Taxes and Home Insurance: These are often held in an escrow account and paid as part of your monthly bill (The Barge Group can help with Home Insurance).

- Maintenance and Utilities: A January home insurance review is a great time to ensure your dwelling coverage reflects current rebuild costs, which have risen along with labor and material prices.

- VA Funding Fee: Unless you have a service-connected disability, most VA loans require a funding fee, which can often be rolled into the loan amount.

We are here to help!

The 2026 housing market near Fort Bragg is all about making “decision-driven” moves rather than emotional ones. VA loans provide the foundation for that stability, offering military buyers in Fayetteville a way to secure a home with no down payment, lower interest rates, and the protection of the VA’s oversight.

Whether you are looking for the historic charm of a bungalow in Haymount, a newer build in the Jack Britt district, or a quiet lot in Hope Mills, your VA benefit is designed to make that transition possible. We aren’t just looking at square footage; we’re looking at helping you build a life here in North Carolina.

Contact Us

Are you ready to explore your options for VA loans in 2026? Whether you’re just starting your PCS planning or you’re ready to schedule a virtual tour, our team is here to help you navigate the Fayetteville market with clarity and confidence.

Contact The Barge Group today to request a custom market snapshot or a “buy vs. rent” analysis tailored to your specific rank and timeline. Let’s make your move to Fayetteville a smooth one!